When Is the Best Time to Buy a Home?

Many buyers ask the same question: When is the best time to buy a home?

Some wait for interest rates to drop. Others hope prices will come down or that more inventory will hit the market. While those factors do matter, the truth is that the best time to buy is not the same for everyone.

The best time to buy a home is when you are financially prepared, your goals are clear, and the move makes sense for your lifestyle.

It Starts With Your Finances

Before buying a home, it is important to look at your overall financial picture. A home purchase involves more than just the down payment. Buyers should also think about closing costs, moving expenses, inspections, and having some reserves set aside for unexpected repairs or maintenance.

A common guideline is to keep your total housing costs at about 25% to 30% of your gross monthly income. Another traditional benchmark is about 28% of gross monthly income toward housing expenses, though some loan programs may allow a little more. Housing expenses include more than just principal and interest. You also need to account for property taxes, homeowners insurance, HOA fees if applicable, and sometimes mortgage insurance.

It is also smart to look at your payment from a comfort standpoint, not just a lender-approval standpoint. Just because you qualify for a certain amount does not always mean that payment feels comfortable for your lifestyle.

Look at Your Total Monthly Debt

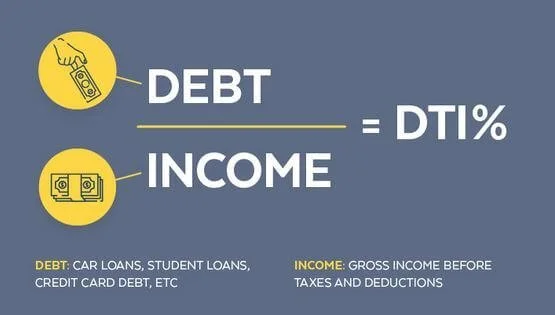

Lenders also look at your debt-to-income ratio, often called your DTI. This is the percentage of your gross monthly income that goes toward all monthly debt obligations combined. That includes your housing payment along with things like car loans, student loans, minimum credit card payments, and other recurring debts.

A traditional benchmark is to keep total monthly debt around 36% of gross monthly income or less, although some buyers may qualify with higher ratios depending on the loan program and their overall financial profile.

That is why buying a home is not only about whether you can qualify. It is also about whether the payment still leaves room in your budget for everyday living, savings, travel, kids, hobbies, or the other priorities that matter to you.

Income and Stability Matter Too

Buying a home is a major financial commitment, so job and income stability play an important role. If your income is steady and your employment situation feels secure, you may be in a stronger position to move forward.

This does not mean everything in life has to be perfect. Very few people ever feel completely ready. But it does help to have enough financial stability that your purchase feels like a smart step, not a stressful one.

Think About Where You Are in Life

The best time to buy also depends on your personal stage of life. For some, it may be the right time because they are tired of renting and want to start building equity. For others, it may be because they need more space, want a different location, are downsizing, or want a home that better fits their day-to-day lifestyle.

Buying a home should support your goals, not complicate them. If owning a home would bring more stability, convenience, or long-term value to your life, that may be a sign the timing is right.

How Long Do You Plan to Stay?

Another important question is how long you expect to stay in the home. If you plan to move again in a year or two, buying may not always make the most financial sense. But if you are planning to stay put for a while, homeownership may offer more long-term benefits.

The longer you stay in a home, the more opportunity you may have to benefit from equity growth and offset the upfront costs that come with buying.

Don’t Get Stuck Waiting for the “Perfect” Market

It is easy to put off buying while waiting for the market to feel more favorable. Many buyers say they are waiting for lower rates, lower prices, or the perfect home to come along. While it is wise to be thoughtful, trying to time the market perfectly can keep people stuck longer than necessary.

No one can predict exactly what rates, prices, or inventory will do next. The market will always have pros and cons. What matters most is whether the purchase makes sense for you personally and financially.

In many cases, buyers who are prepared and focused on their own goals make better decisions than buyers who wait for ideal market conditions that may never fully appear.

The Right Time Is Personal

There is no one-size-fits-all answer to the question of when to buy a home. The right timing depends on your finances, your goals, your comfort level, and the kind of life you want your home to support.

A lender can tell you what you may qualify for, but only you can decide what feels comfortable for your budget and your life.

The Bottom Line

The best time to buy a home is not when headlines say it is the perfect market. It is not when rates hit a certain number or when someone else says you should make a move.

The best time to buy is when it is right for you.

When your finances are in order, your goals are clear, and the purchase fits your life, that is when buying a home can make the most sense.